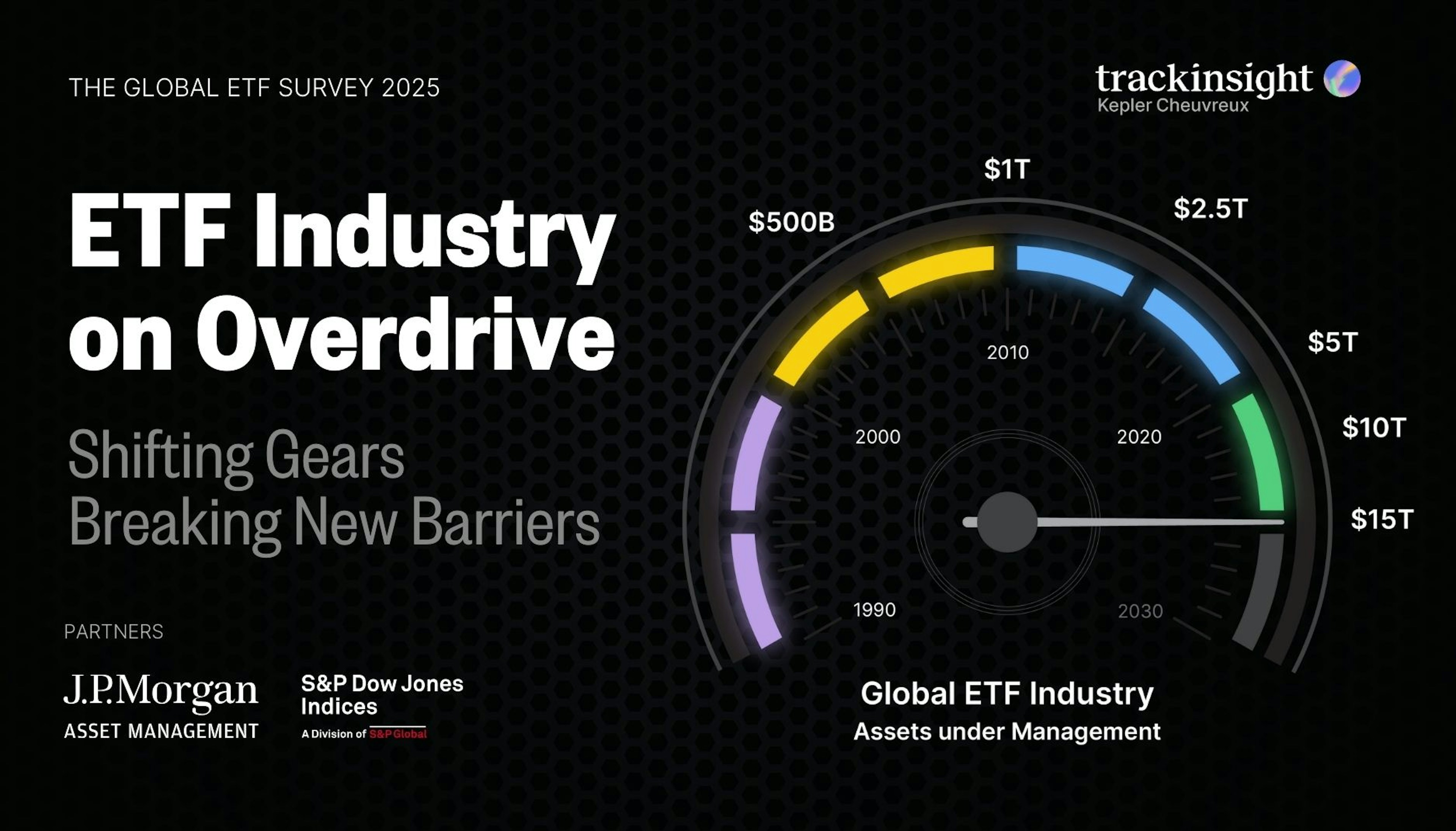

O que o relatório inclui

- 600+ investidores (US$ 1,1 tri em ETF)

- Tendências quentes: renda fixa, cripto, ESG

- 80+ previsões para 2025

Fixed Income Investing: A Guide to Bond ETFs

Over the last decade, bonds have proven to be a valuable addition to investors’ portfolios. More than just an alternative to equities, they are an efficient tool to balance risk in your portfolio and help you navigate a wide range of markets. This guide is designed to introduce you to the vast world of fixed income, that you can access easily and at a low-cost with bond ETFs.

What is a bond?

While a share gives you ownership of part of a company, a bond is a debt that a company or government can issue/sell to raise money. When you invest in a bond, you are effectively loaning money to the issuer with the promise that they will repay you (with interest) down the line. Unlike stocks, most bonds have a determined lifetime. At the end of the security life (when bonds reach ‘maturity’), the amount borrowed is reimbursed and all interests are paid.

Publicidade

Bonds are useful to diversify your portfolio. They are different from stocks and they exhibit limited historical correlation with them. This diversification is good for your portfolio, it allows you to average out the specific risk that comes from your equity holdings.

They are also often considered less risky than stocks because of their nature. Bonds are called ‘fixed income’ instruments because they have scheduled coupon and principal payments. This characteristic lowers the incertitude around your investment outcome and makes bonds price more stable.

Characteristics of a bond

Bonds are often defined by their maturity, issuer, coupon, type, and credit quality. Before investing in bonds ETF, it is important to understand each of the characteristics of a bond.

Maturity

A bond’s maturity is the date at which the bond stops existing. It means that at this date, all payments (interest and principal) have been made to the investor by the bond issuer.

Maturities can vary and can be classified as such:

- Money Market – for instruments maturing in less than a year

- Short Term – for instruments maturing between 1 and 5 years from now

- Intermediate-Term – for instruments maturing between 5 and 10 years from now

- Long Term – for instruments maturing in more than 10 years

- Perpetual instruments – for instruments that do not mature

Coupon

The interests that bond investors earn during the life of the security are called “coupons”.

There are different types of coupons, mainly:

- Fixed rate coupon – they are the simplest bonds, the coupon is the same amount throughout the life of the bond

- Floating rate coupon – they vary and are linked to a reference rate (e.g., LIBOR) the coupon resets at a pre-defined frequency

- Zero coupon – these bonds do not pay any coupon but their price reflects the theoretical coupon as they trade at a price lower than their nominal value

- Step-up coupon – the coupon changes to some determined values at certain points of the bond’s life

- Inflation-linked coupon – the coupon is linked to a Consumer Price Index (CPI) in order to protect investors against inflation

Nominal

The nominal value of a bond is the value the issuer will have to pay back. It is also called the bond’s par, principal, or face value. The nominal value is different from the price of a bond. Indeed, when a bond trades at the same price as its nominal value, we say the bond is “at par”. When its price is below par, we say the bond is trading at a discount. Finally, when the price of the bond is higher than its nominal, we say the bond trades at a premium. This happens when interest rates go down for example and bonds with higher coupons become more interesting for investors.

Publicidade

Credit Rating

A bond’s credit rating is one of its most important characteristics. This score assesses the creditworthiness of the bond issuer. Bonds, just like issuing companies and governments, are rated by agencies such as Standard and Poor’s (S&P) or Moody’s. Even though different agencies have different methodologies of rating companies and different classifications, those scores can be compared.

The highest credit rating is AAA, which mainly represents government bonds or tech leaders such as Microsoft. The lowest credit rating is D, which basically means the company is in a state of default.

Bonds issued by companies or governments rated from AAA to BBB- are called “investment-grade” and those rated below BBB- are called “high yield” or “junk bonds”. Companies with a lower credit rating typically offer a higher yield and trade at a discount to par.

Issuers

Companies are not the only ones that can issue bonds. Governments and other related entities can also issue bonds to finance their projects.

Government Bonds

Government bonds are issued by sovereign entities as their primary means of funding. They are also referred to as “government debt” or “treasuries”. Government bonds issued by the US are often viewed as risk-free instruments and have the highest credit ratings. Most government bonds are considered investment grade; however, some emerging countries' bonds are riskier, and their creditworthiness is a function of the Debt to GDP ratio of the country, and the strength of the currency in which the bond is denominated. Supranational entities such as development banks can issue bonds.

Municipal Bonds

Municipal Bonds are bonds issued by cities, states, or municipalities to fund projects such as the construction of a mall or a highway. Municipal bonds are repaid through taxes, or revenues earned by a project. Some municipal bonds also attract investors because they are tax-free. Even though most municipal bonds are often classified as investment grade, high yield municipal bonds also exist.

Corporate Bonds

Corporate bonds are issued by companies in need of cash to finance their growth or project. Unlike stocks, bonds do not give the investor ownership of the company. However, if the company were to be liquidated, bondholders have a higher claim to the company’s assets than shareholders. Credit rating of the bond is a very important characteristic of corporate bonds as they are riskier than government and municipal bonds.

Other types of Bonds

Regular bonds pay coupons based on a fixed or floating rate, but there are also some special types of bonds with unique characteristics, such as covered bonds, asset-backed securities (ABS), mortgage-backed securities (MBS) and convertible bonds.

Publicidade

Covered Bonds

Covered Bonds are bonds issued by financial institutions that are collateralized (covered) against a pool of assets. It works like a guarantee. If the issuer defaults, the pool of collateral assets will be sold, and the cash proceeds will be used to pay what the investor owes.

Asset-backed securities (ABS) and Mortgage-backed securities (MBS)

Asset-backed securities (ABS) and Mortgage-backed securities (MBS) are a special type of covered bonds pooled and collateralized by physical assets. MBS pool numerous mortgages into one bond and the underlying properties act as assets backing the security. Coupons are paid from monthly mortgages payments. MBS are typically issued by US government agencies such as Federal National Mortgage (FNMA or Fannie Mae), and Federal Home Loan Mortgage Corp. (Freddie Mac).

Convertible Bonds

Convertible Bonds are corporate bonds that can be converted into the company stock during their life. If the bond reaches its maturity without having been converted, the investor loses its right to conversion. Convertibles offer a higher upside potential than regular bonds because of this special feature, so they often have a lower coupon. If the company performs better than expected, investors can profit by converting their bonds into equity.

Yield To Maturity (YTM)

The Yield To Maturity (YTM) is the annual rate of return an investor would get if they held the bond until maturity. It is therefore the internal rate of return (IRR) of the bond. The yield to maturity is directly connected with the price of a bond. Indeed, we have 3 cases:

- Yield to maturity = coupon rate à Nominal value > Bond price (par bond)

- Yield to maturity > coupon rate à Nominal value > Bond price (discount bond)

- Yield to maturity < coupon rate à Nominal value < Bond price (Premium bond)

Duration

The duration is an abstract concept that many investors find difficult to grasp. In this article, we will leave beside the mathematical explanation and focus on the interpretation of duration.

Bonds prices move in opposite direction with interest rates. When interest rates rise, bonds prices fall, and the opposite when interest rates fall. Duration is the measure of the sensitivity of the price change to an interest rate change. For example, for a given rise in interest rates, a bond with a higher duration will see its price drop further than a bond with a lower duration.

Generally, bonds with longer maturities and lower coupon rates have higher durations. This means their price is more sensitive to changes in interest rates.

Convexity

If duration is an abstract concept, convexity is an imaginary concept. Let’s try to keep things as simple as possible here.

Duration calculates the price sensitivity of bonds to a change in interest rates based on a linear relationship. However, the relationship between yield and price is not linear. Therefore, there will be a small difference in the price change given by the duration effect and the actual change in price.

Convexity is a measure of the non-linearity of the relationship and is intented to correct this small difference. The sum of the duration effect and the convexity effect gives the percentage change in price for a given change in interest rates.

Professionals use these concepts as risk management tools. However, personal investors will rarely need to go this deep into risk management.

What are Bond ETFs? Advantages & Limits

Advantages of Bond ETFs

Cheap and easy diversification tools

ETFs are a powerful tool when it comes to diversification. Bond ETFs are comprised of many bonds and therefore are already diversified. They also are cost-efficient, for the same level of diversification, ETF fees are way lower than what you would pay buying each instrument one by one. Especially when it comes to bonds, reaching a diversified portfolio can be rather expensive.

No maturity dates

Unlike individual bonds, ETFs made of bonds do not mature, making portfolio management easier for investors as they don’t have to worry about laddering their bonds portfolio.

Enhanced liquidity

Enhanced liquidity is another key advantage of bond ETF compared with individual fixed income securities. Bonds tend to be less liquid than stocks, especially as their maturity approaches. Bond ETFs trade like stocks, which offers great liquidity to investors. Moreover, Authorized Participants are chosen by the ETF manager to ensure liquidity. They have the power to create and redeem shares and therefore provide liquidity to investors.

Limits of Bond ETFs

Besides the upsides of Bond ETFs, there are some limits to be stated, here are the main:

Expense ratios

Because bonds are safer than stocks, their potential return is also limited compared with stocks. For this reason, Bond ETFs’ expense ratio can be relatively high.

No principal payments

An attractive characteristic of bonds is that when they mature, the principal is paid back to you which offers a kind of capital guarantee in case of rise of interest rates (so decrease of bonds prices). Most Bond ETFs do not mature, and therefore do not repay principal. One can argue it is fair since you pay the ETF cheaper than what you would pay for a bond. Also, if you are looking for this feature of bonds, maturing ETFs exist such as the iShares iBonds Dec 2027 Term Corporate ETF. They work just like a bond in terms of cash flows and provide the liquidity and transparency of an ETF.

Indirect currency risk

Some ETF may invest in securities denominated in different currencies. By investing in these ETFs, you indirectly get exposed to currency risk (changes in exchange rates between currencies). If you don’t want to bear any currency risk, some share classes are hedged to specific currencies.

What are Active Bond ETFs and Passive Bond ETFs?

To create an efficient bonds portfolio, investors need to react quickly to market conditions. Indeed, to catch fixed income opportunities in the market, investors have to navigate through the asset class and invest in appropriate securities depending on the state of the economy.

As for equity, bonds indexes are not optimized, and their performance highly depends on the construction methodology. However, unlike stocks, bonds prices are less volatile thanks to scheduled cash flows.

The points elaborated above make up the rationale behind the development of many fixed income active ETFs. Keeping your portfolio up to date can be challenging and time-consuming, especially if you are not familiar with the world of fixed income. If you have little time to spend on managing your bond portfolio, active bond ETFs can be the right alternative for you.

Active bond ETFs work just like passive bond ETFs, with the exception that a dedicated professional investment management team oversees the fund’s efficiency. They use their knowledge and experience to create bonds portfolios that correctly respond to market conditions.

Typically, this means they allocate a bigger portion of the portfolio in higher yielding securities when markets are favorable (i.e., bullish) and retreat towards government securities such as US treasuries when markets become wavy (i.e., bearish).

Unlike passive bond ETFs, active bond ETFs are optimized and adapt to markets conditions. However, the performance of the fund is linked to the competence of the portfolio managers, before investing, investors should run a background check on the past performance of the fund compared with its benchmark.

Of course, the expertise of the management team comes at a price, investors will pay a higher fee compared with passive ETFs.

Find bond ETFs with Trackinsight’s ETF screener.

Mais conteúdos educativos

Sobre o Trackinsight

Trackinsight é um fornecedor líder de dados e tecnologia sobre ETFs, capacitando instituições a tomarem decisões informadas na seleção de ETFs, construção de portfólios e otimização.

Desde a nossa fundação em 2016, estamos na vanguarda da indústria, oferecendo ferramentas acessíveis, abrangentes e confiáveis para apoiar as necessidades em constante evolução dos investidores.

Ao longo da última década, a Trackinsight expandiu suas operações em seis países, atendendo milhares de investidores profissionais. Temos inovado consistentemente para fornecer soluções de ponta que atendam às demandas em mudança do mercado de ETFs.

Em 2024, a Kepler Cheuvreux, uma importante empresa independente de serviços financeiros europeia, adquiriu uma participação majoritária na Trackinsight, tornando-se o principal acionista da empresa.

Essa parceria estratégica solidifica a posição da Trackinsight como um fornecedor de destaque de ferramentas de seleção e análise de ETFs, enquanto fortalece o compromisso da Kepler Cheuvreux em se tornar um jogador de destaque no setor de ETFs.

Juntos, estamos comprometidos em oferecer serviços avançados que capacitem investidores profissionais, consultores, instituições e emissores. Este novo passo nos permite fornecer soluções tecnológicas ainda mais abrangentes e inovadoras, levando o investimento em ETFs a novos patamares.

Mais sobre o TrackinsightFerramentas ETF

PLATAFORMA

Notícias e pesquisas sobre ETFs

SOLUÇÕES PROFISSIONAIS

SOLUÇÕES PARA

Política de privacidade | Política de bolachas | | Termos de uso | Impressão