Global ETF Survey 2026: Answer now →

Help us improve your experience. Please confirm your investor type:

Don’t Miss a Move in the ETF Market

Sign up and keep track of everything that moved the ETF industry this week. From new launches to regulatory shifts across the Atlantic.

The fundamentals of high yield debt for the year ahead

The end of 2022 marked the 7th consecutive interest rate hike for the FED, along with a change in tone from FED officials. With the end of the hiking cycle in view, and a prolonged period of higher rates, we explore the fundamentals of high yield debt for the year ahead, and its role in investors’ portfolios.

By Daniel Chivu

January 20, 2023

Advertisement

Although there is no doubt that we are in an uncertain economic environment, employment and wage trends remain positive across North America, while in Europe, Germany recently recorded a faster drop in inflation than predicted. The odds of a so-called soft landing are rising globally, though we are certainly not out of the woods yet, especially with broader equity markets looking weak to start the year.

The high yield bond market however is showing some promise in the face of better-than-feared economic conditions. Here we’ll take a closer look at 3 factors that could likely play in its favor.

1. Stronger Fundamentals and lower debt issuance

The economic backdrop is expected to remain soft over the first half of 2023, as compared to the previous 12 months, but employment trends will likely mitigate the effects of a potential recession. On the other hand, high yield as an asset class is stronger than it has been over the last year with yield spreads at 4.81% as of Dec 31st 2022, far surpassing the value from a year earlier (3.1%).

Options Adjust Spreads (OAS), also referred to as Credit Spreads are the primary way of measuring the risk-return metrics of high yield debt, by comparing it to the risk-free rate, usually U.S Treasuries. The higher the spread, the higher the difference between the two, making for a more attractive high yield opportunity for the same unit of risk. Wider spreads however, are usually associated with economic hardship.

📊 Share your ETF outlook

From AI infrastructure to active strategies, the ETF landscape is shifting. Share your perspective in the 7th Annual Global ETF Survey and get exclusive early access to the final report.

Figure 1: US High Yield Master II Option-Adjusted Spread

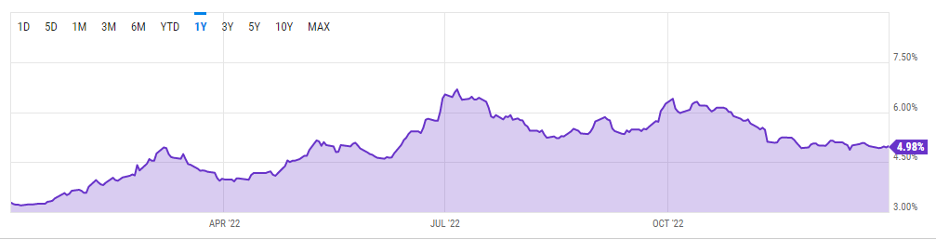

European high yield spreads are exhibiting a similar pattern, with the spread as of Dec 31st sitting at 4.98% compared to 3.31% a year earlier:

Figure 2: Euro High Yield Index Option-Adjusted Spread

It should be noted, however, that although an obvious widening has occurred since the beginning of 2022, the spreads for both U.S and European high yield bonds began flattening out and exhibiting a slightly downward trajectory starting in October, signaling a belief that a soft landing is still on the cards.

Lower debt issuance is also a positive factor for high yield in the years ahead. With most corporate capital raising and refinancing done in 2021 at ultra low rates, firms are not expected to require new funding until 2025. This means a low probability of further high-yield debt issuance in the year ahead, which would lower the effective yield as the supply rises.

As of August 2022, about U.S. $92 billion of high yield issuance occurred, compared to $366 billion for the same period in 2021, as per Capital Group.

2. Default rates have been low

Another factor likely to support the outperformance of high yield debt in the year ahead is the historically low default rates we have noticed so far.

As of July 31st 2022, default rates were at 1.1%, far below the 3.1% historical average, as the following chart from J.P Morgan shows:

Fitch Ratings on the other hand expects a slight increase in defaults in 2023, in the range of 2.5%-3.5%, and they calculate a historical default rate of 3.8%, as opposed to J.P Morgan’s 3.1%.

Either way, defaults are not expected to jump to the elevated levels seen in 2020, and will most likely be in line with 2019’s numbers, which did not see any underperformance in common high yield ETFs, but rather a flat or slightly positive year (see HYG, SPHY).

3. Energy fundamentals strongest in the last decade

Traditionally, the Telecommunication and Energy industries have made up a large part of high yield debt issuance, with the aforementioned ETFs (HYG, SPHY) having between 25-30% of their holdings in these two industries.

With the significantly improved energy fundamentals over 2022, which are projected to continue over the next 12 months at least, the probability of default on the underlying debt decreases drastically. Many companies are flushed with cash as a result of the higher prices over the last 12 months, and are retiring debt early, or reassuring investors of their ability to service their debt in the years to come.

Capital expenditures are expected to remain low by historical standards, and cash flows will be directed towards debt payments or dividends, ensuring long term profitability from their outstanding bonds.

There is also the possibility of a re-rating in their underlying debt, which would further benefit investors in the form of appreciation in the bond prices.

Advertisement

The bottom line

High yield debt is well positioned to have a strong year in 2023 and beyond, given the above factors remain constant.

The time horizon on high yield is equally important to the sector allocation, as historical data shows. A time horizon of +5 years is associated with outperformance 94% of the time:

Therefore, the goal with investing in high yield debt is to gain exposure to companies that are inherently lower quality, while at the same time receiving constant cash flow in order to be compensated. It is a strategy that works in the medium to long term, provided that adequate diversification occurs, and should be considered as a part of investors’ portfolios going into the new year.

Please note this article is for information purposes only and does not in any way constitute investment advice. It is essential that you seek advice from a registered financial professional prior to making any investment decision.

More articles

About Trackinsight

Since our founding in 2016, we have been at the forefront of the industry, delivering accessible, comprehensive, and reliable tools to support the evolving needs of investors.

Over the past decade, Trackinsight has expanded its operations across six countries, serving thousands of professional investors. We’ve consistently innovated to provide cutting-edge solutions that meet the changing demands of the ETF market.

In 2024, Kepler Cheuvreux, a leading independent European financial services firm, acquired a majority stake in Trackinsight, becoming the company's principal shareholder.

This strategic partnership solidifies Trackinsight's position as a premier provider of ETF selection and analysis tools, while strengthening Kepler Cheuvreux’s commitment to becoming a leading player in the ETF sector.

Together, we are committed to offering advanced services that empower professional investors, advisors, institutions, and issuers. This new step enables us to deliver even more comprehensive and innovative technological solutions, driving ETF investing to new heights.

More about TrackinsightETF TOOLS

PLATFORM

ETF NEWS & RESEARCH

Privacy policy | Cookie policy | | Terms of use | Imprint