Global ETF Survey 2026: Answer now →

Help us improve your experience. Please confirm your investor type:

Don’t Miss a Move in the ETF Market

Sign up and keep track of everything that moved the ETF industry this week. From new launches to regulatory shifts across the Atlantic.

Economic hegemony remains U.S. top priority

In a post-Covid world where Chinese economy has recovered, the main U.S. priority will be to maintain its economic hegemony for as long as possible.

By Christophe Barraud

June 21, 2021

- United States

- China

Advertisement

In a post-Covid world where Chinese economy has recovered quickly, recent developments suggest that the main U.S. priority is to maintain its economic hegemony for as long as possible. This ambition has prompted U.S. Congress to pass three stimulus packages in less than twelve months. The goal is not simply to return to the pre-crisis level of activity, but to return to the pre-Covid growth trend. In parallel, the Biden administration has completely revised its foreign policy strategy. The aim is to re-establish strong relationships with key trading partners such as Europe to create an alliance that will limit China's economic and geopolitical ambitions.

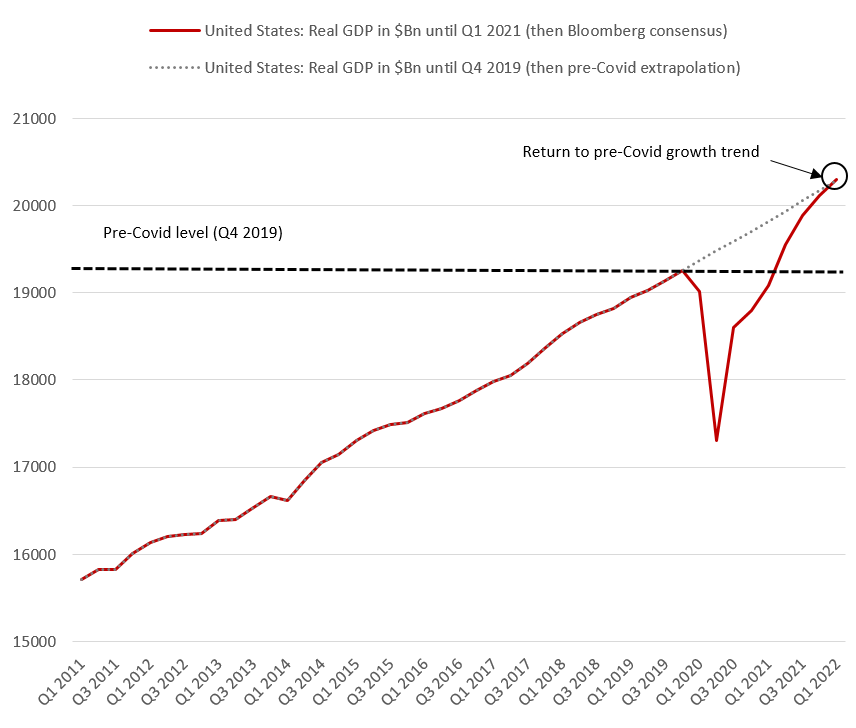

Towards a return to the pre-Covid growth trajectory from Q1 2022

Faced with the economic shock caused by the Covid-19 pandemic, the U.S. authorities chose to respond on a monetary level with a rapid increase in the Federal Reserve's asset purchases, but above all on a fiscal level with an ultra-expansionist policy. In less than twelve months, U.S. Congress has approved three stimulus packages totalling nearly $5 trillion, or nearly 25% of nominal GDP, as highlighted in an IMF study. In this context, on a QoQ annualized basis, U.S. growth rebounded strongly in Q3 2020 (+33.4%) and kept rising in Q4 2020 (+4.3%) and Q1 2021 (+6.4%). The latest fiscal stimulus voted in March (~$1.9 trillion) should logically result in an acceleration of the dynamic in Q2 2021 (+10% expected) and still sustained growth rates at least until Q1 2022 (+7% in Q3 2021, +4.9% in Q4 2021 and +3.5% in Q1 2022 according to the Bloomberg consensus)

📊 Share your ETF outlook

From AI infrastructure to active strategies, the ETF landscape is shifting. Share your perspective in the 7th Annual Global ETF Survey and get exclusive early access to the final report.

The U.S. economy should benefit from a near-total easing of health restrictions by mid-July, while new checks to families with at least one child are expected at the same time. In the meantime, a likely rebound in international mobility (thanks to the vaccine passport) and the forced savings accumulated since March 2020 (potentially 15/20% of excess savings[1]) should support activity. Thus, the U.S. economy is expected to return to its pre-crisis real GDP by Q2 2021 and return to its pre-Covid growth trajectory by Q1 2022.

Similarly, despite fears of a surge in inflationary pressures (which seems to be secondary to the U.S. officials), new measures should rapidly emerge. Firstly, it should be noted that the "Innovation and Competition Act", which is expected to inject $250 billion over a period of five years (2022[2]-2026), could be validated within a few weeks. Finally, a new infrastructure spending plan (of at least $1 trillion) remains one of the Biden administration's priorities and could be voted by the end of September/beginning of October. This could be spread over eight years with a concentration of spending in the first five years.

Towards an international alliance to curb Chinese ambitions

As he pledged during his campaign, Joe Biden wants to abandon the unilateral confrontation driven by Donald Trump against China. The Biden administration's strategy is clearly to rebuild strong relationships with key trading partners such as Europe to create an alliance that will limit China's economic and geopolitical ambitions.

In this respect, the latest developments between the U.S and Europe are clearly a case in point. The Biden administration has made many compromises and extended its hand to Europe in many and varied areas. As a first step, both sides agreed to suspend for five years the punitive tariffs they were imposing on each other in the Airbus-Boeing dispute. A partial truce on metal tariffs has also been introduced until the end of the year.

At the same time, the idea of sanctions linked to the inauguration of the Nord Stream 2 pipeline has been ruled out by the Biden administration. Similarly, the U.S. authorities are keen to find a solution to revive the Iranian nuclear deal (which would benefit France, Germany and the UK).

On the fiscal front, the U.S. seems to be working towards an international agreement on the taxation of the tech giants. Lastly, on the climate front, with just a few months to go before Cop26 in Glasgow, the U.S. has made the fight against global warming a major development axis, in line with European ambitions.

In this context, it is not surprising that Europe has chosen to put its investment agreement with China on hold. At the same time, European leaders supported a global infrastructure plan at the G7 to help disadvantaged countries and to compete with Beijing's "New Silk Roads".

As a conclusion, it appears that economic hegemony remains U.S. top priority, which will have significant implications. Firstly, the risk of inflationary pressures is likely to be treated as a secondary concern. In other words, the U.S. authorities will not hesitate to spend again despite the $5 trillion put on the table in less than twelve months. In parallel, relations between China and countries that support U.S. initiatives will deteriorate, further fuelling tensions between the U.S. and China. As an example, one can imagine that if the European Commission gave the green light to an investment agreement between the EU and Taiwan, China would take it as an affront.

Advertisement

[1] In April, total excess savings (accumulated since March 2020) reached $2.330 trillion (>10% of nominal GDP).

[2] The 2022 fiscal year begins on October 1st 2021.

Chief Economist and Strategist at Market Securities since 2011, Christophe Barraud has been awarded by Bloomberg the title of Top Forecaster of the U.S. Economy (2012-2020), Eurozone Economy (2015-2019) and Chinese Economy (2017-2020). He also won the Forecaster of the Year contest organized by MarketWatch in 2020.

Advertisement

More articles

About Trackinsight

Since our founding in 2016, we have been at the forefront of the industry, delivering accessible, comprehensive, and reliable tools to support the evolving needs of investors.

Over the past decade, Trackinsight has expanded its operations across six countries, serving thousands of professional investors. We’ve consistently innovated to provide cutting-edge solutions that meet the changing demands of the ETF market.

In 2024, Kepler Cheuvreux, a leading independent European financial services firm, acquired a majority stake in Trackinsight, becoming the company's principal shareholder.

This strategic partnership solidifies Trackinsight's position as a premier provider of ETF selection and analysis tools, while strengthening Kepler Cheuvreux’s commitment to becoming a leading player in the ETF sector.

Together, we are committed to offering advanced services that empower professional investors, advisors, institutions, and issuers. This new step enables us to deliver even more comprehensive and innovative technological solutions, driving ETF investing to new heights.

More about TrackinsightETF TOOLS

PLATFORM

ETF NEWS & RESEARCH

Privacy policy | Cookie policy | | Terms of use | Imprint