Global ETF Survey 2026: Answer now →

Help us improve your experience. Please confirm your investor type:

The Ultimate ETF Comparison Tool - Try Now!

Analyze up to 5 ETFs side-by-side and gain instant insights on performance, fees, holdings, and more to make data-driven investment decisions.

Investing in the Core Materials Powering the Green Tech Revolution

The future of green tech isn’t in the sky or the wind. It’s in the ground.

By Ben Taylor

February 24, 2023

Advertisement

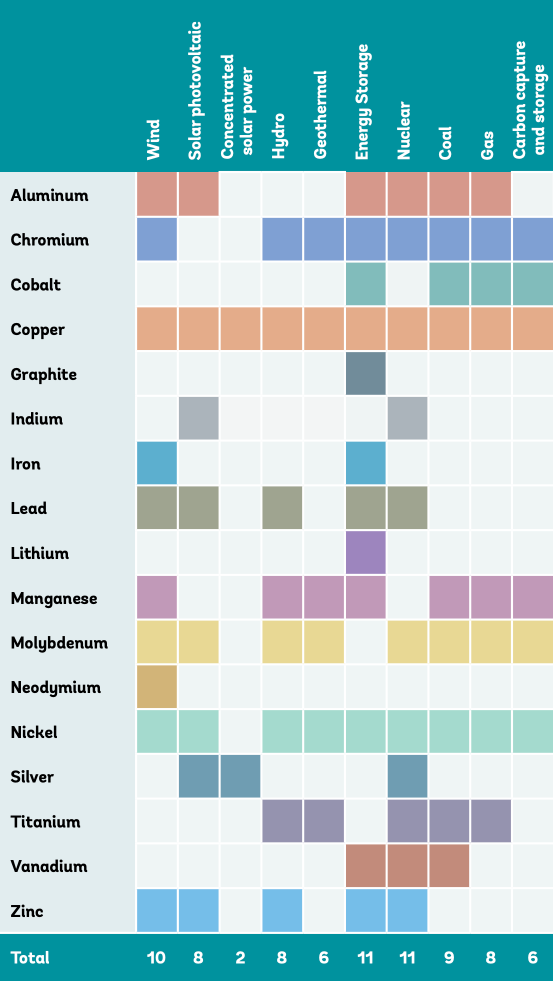

The green tech revolution is making sustainable energy possible. Wind power, solar power and battery technology are all part of the plan. But making that plan work is going to require an enormous amount of in-ground material.

Consider zinc. It is used to coat solar panels and wind turbines to prevent rust. It is also a key component in zinc-ion batteries and the galvanized steel used in EV car bodies. While naturally abundant, it still needs to be mined and processed.

ETF Data Built for Precision

Trackinsight delivers reliable and comprehensive coverage on 14,000+ ETFs

Aluminum is also a must. The green tech revolution is going to demand much more of it. In fact, demand for aluminum is estimated to increase by 26% from current levels according to Morgan Stanley Research.

Titanium, lithium, copper, nickel, silicon, and graphite are all also on the menu. Demand will rise across all of these materials. Research from the International Energy Agency projects that the transition to green tech could lead to a 40-fold increase in lithium consumption by 2040. Demand for graphite, cobalt, and nickel could increase 20 to 25 times over the same period.

Here, we look at the three trends in green tech that will position material and mining companies to outperform in the coming years.

Material Intensity is Rising

Green power generation and road transport will require more materials than ever. Consider that generating one terawatt-hour of electricity from solar and wind demands 300% and 200% more metals than what’s required for generating the same amount of power from a traditional gas-fired power plant according to research from McKinsey.

The demand for materials needed to build these green solutions will soar. In some cases, the demand will become so high that the technology will need to evolve so that substitutions can be made. But even in this scenario, the major mining companies will be the solution. Why? Because those substitution materials will also need to be pulled from the ground.

Consider the example of cobalt. Originally the metal was a common component in batteries. As demand surged and supply remained limited, engineers developed batteries that could rely more on nickel in place of cobalt.

In short, even as substitution materials find their way into manufacturing, the mining and material companies are still the primary source for the core components of green tech.

Advertisement

Green Tech Demand is Now Global

The demand for the materials powering green tech will be robust and sustained because it is global. To date, 189 countries have joined the 2015 Paris climate accord. The intention of the agreement is to keep global warming under 2C. As a result, many of these countries are racing to reduce fossil fuels and accelerate clean energy transitions.

As recently as 2021 global investment in green tech reached $755 billion up 27% relative to 2020. China increased its total wind and solar capacity by 19%.

Other regions are making equally impressive commitments. In fact, this trend has been unfolding over the past several years and is forecasted to grow. Between 2016 and 2021 Africa, Australia, China, Europe, India, Japan, Latin America, the Middle East, Southeast Asia, and the US have all increased their average yearly installed capacity of solar and wind.

One of the best examples of the global spread of green tech solutions is a project called the Sun Cable which aims to connect renewable energy in Northern Australia with Southeast Asia. In doing so, the plan will unite the world's largest solar plant, the world's largest battery, and the world's longest submarine power cable. Projects like this can be found across the globe and they will all demand more green tech metals and materials.

Green Tech Demands Recyclable Materials

Meeting the massive demand for green tech metals means developing technologies that use recyclable materials.

Though industries can begin to recycle certain metals now, that alone will not be enough. Therefore, mining companies will become crucial because they alone have the power to target these specific metals and bring them to the market for repeated use.

The most sought-after metals will likely be copper, cobalt, nickel and lithium all of which can be recycled almost infinitely. It’s no surprise that a study from Belgium's KU Leuven University forecasts that 40% to 75% of Europe’s green tech metal needs could be met through recycling by 2050.

The recyclability of these metals will only drive up demand. As consumers increasingly adopt green tech solutions, manufacturing will need more of the materials that are part of the ecosystem. This is also true of industrial-scale government-funded projects that will need replacements and upgrades as they age.

Advertisement

How to Invest in Green Tech

One way investors can benefit from the increasing demand for these materials is with Amundi's S&P Global Materials ESG UCITS ETF (WELI).

More than 99% of the holdings are part of the materials sector. Many of the companies in the top 10 holdings are mining corporations that will be integral to meeting the global demand for lithium, copper, nickel, aluminum, graphite, and more.

With a total expense ratio of 0.18% it is one of the more affordable options available.

The answer to a sustainable future is right under our feet. Forward-thinking investors are taking this opportunity to invest in the future.

*IMPORTANT: The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Trackinsight. Past performance is not indicative of future results. Investors should undertake their own due diligence and carefully evaluate companies before investing. ADVICE FROM A FINANCIAL PROFESSIONAL IS STRONGLY ADVISED.

More articles

About Trackinsight

Since our founding in 2016, we have been at the forefront of the industry, delivering accessible, comprehensive, and reliable tools to support the evolving needs of investors.

Over the past decade, Trackinsight has expanded its operations across six countries, serving thousands of professional investors. We’ve consistently innovated to provide cutting-edge solutions that meet the changing demands of the ETF market.

In 2024, Kepler Cheuvreux, a leading independent European financial services firm, acquired a majority stake in Trackinsight, becoming the company's principal shareholder.

This strategic partnership solidifies Trackinsight's position as a premier provider of ETF selection and analysis tools, while strengthening Kepler Cheuvreux’s commitment to becoming a leading player in the ETF sector.

Together, we are committed to offering advanced services that empower professional investors, advisors, institutions, and issuers. This new step enables us to deliver even more comprehensive and innovative technological solutions, driving ETF investing to new heights.

More about TrackinsightETF TOOLS

PLATFORM

ETF NEWS & RESEARCH

Privacy policy | Cookie policy | | Terms of use | Imprint